Components of the TyEL contributions of large employers:

- The TyEL basic contribution, which is the same for all pension insurance companies

- Company-specific expense loading fee

- Premium loss discount

- Client bonus

- Contribution category based on the company’s disability pension expenditure.

Who is considered a large employer?

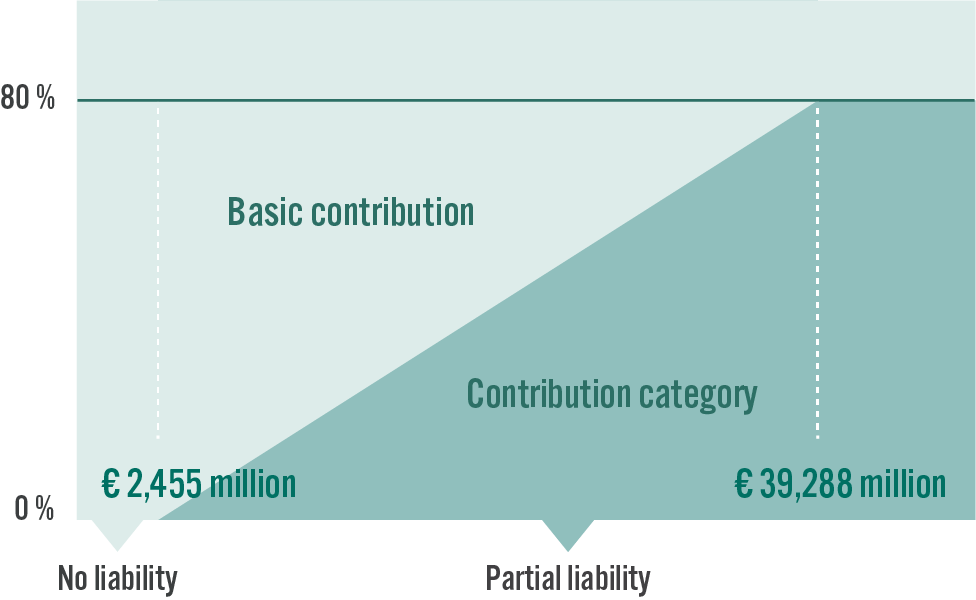

Large employers are companies whose payroll exceeded EUR 2,455,500 in 2024. The disability pension component of the TyEL contribution is comprised of the basic contribution, which is affected by the age distribution of the employees and a liability component in accordance with the contribution category as follows:

- If a company’s payroll was less than EUR 2,455,500 in 2024, the disability pension contribution is determined solely on the basis of the basic contribution without any impact of a contribution category.

- If a company’s payroll was EUR 2,455,500–39,288,000 in 2024, the employer is subject to partial liability up to a maximum of 80%. Up to 80% of the disability pension contribution is determined by the company’s contribution category and the rest by the basic contribution.

- If a company’s payroll exceeded EUR 39,288,000 in 2024, the employer is subject to partial liability of 90%. This means that 90% of the disability pension contribution is determined by the company’s contribution category and 10% by the basic contribution.

The liability rate will decrease gradually over the years 2025–2028.

How is a company’s contribution category determined?

Large employers can affect the amount of their TyEL insurance contributions by promoting the work ability and well-being at work of their employees. The contribution category is determined on the basis of a company’s disability pension cases. Each granted disability pension may affect the contribution category of large employers and, consequently, the amount of their disability pension component.

The disability pension expenditure refers to the costs accrued by an employer for all cases of disability pension granted until further notice. In the future, the disability pension expenditure and consequent contribution category will also be affected by cash rehabilitation benefits that have continued longer than two years (fixed-term disability pensions).

The pension expenditure is affected by the employee’s age, employment history and salary. The pension expenditure will not be debited from the employer as such, but is taken into consideration when determining the contribution category of the employer. If a company has a higher than average disability pension expenditure, its contribution category will also be higher.

Correspondingly, the lower the disability pension expenditure, the lower the contribution category and liability component. It is worthwhile to proactively maintain and support employees to continue at work through, for example, well-being at work or rehabilitation measures. This benefits both the employees and the employer.

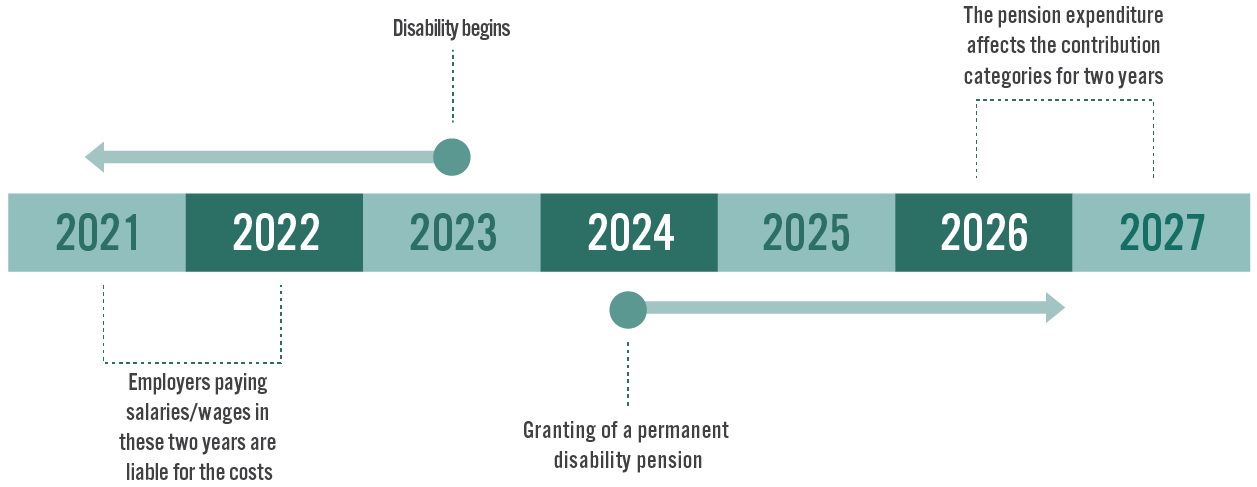

The disability pension expenditure is divided among those employers who have paid wages or salaries to the employee in question during the two calendar years preceding the disability. The year in which the disability pension was granted will determine the time period when the pension expenditure will impact the contribution category. The pension expenditure affects the contribution category for two years.

Contribution categories, risk ratios and coefficients

Starting in 2026, the contribution category will no longer have an impact if the disability has begun more than five years earlier.

If the employee’s employment relationship started with a work trial or apprenticeship training as part of rehabilitation under the earnings-related pension system (vocational rehabilitation), any possible disability will not affect the employer’s contribution category. The protection period is valid for five years and is applicable to employment relationships starting on 1 January 2024 or later. If an employee becomes disabled during the protection period, the employer must remember to notify the pension provider of this as soon as possible. It is the employer’s obligation to report that the employee’s employment relationship started with a work trial or apprenticeship training as part of vocational rehabilitation for a maximum of five years prior to the pension contingency. The notification must be made no later than by 15 November of the year following the year in which the employee retired on disability pension in order to avoid the impact of the contribution category.

Formulation of the contribution category

The process of calculating the contribution category for each employer involves the calculation of risk ratios, the average of which will determine the contribution category. The risk ratio is the ratio between the employer’s own disability pension expenditure and the average disability pension expenditure. Risk ratios are calculated from two years: for 2026, they are calculated from 2023 and 2024. The average of the risk ratios from these two years determines a company’s contribution category.

The aim of the contribution category model is to encourage employers to advance their employees’ well-being at work and work ability, promote the employment of older persons and help extend work careers. In the future, persons hired as new employees over the age of 55 will not have an impact on the contribution category of companies even if they later retire on disability. The change applies to new employment relationships starting on or after 1 January 2024.

Please note: An employee is not considered a new employee if they have worked for the same group of companies during the three previous years. The employer should ensure that the information concerning new employees can be found from the company’s HR system. If an employee develops an inability to work, the employer must remember to notify the pension provider of this as soon as possible. The notification must be made no later than by 15 November of the year following the year in which the employee retired on disability pension in order to avoid the impact of the contribution category.

Similarly, retaining an older employee who has been hired earlier is relatively risk-free from the point of view of the contribution category if the employee is no more than a couple of years away from their personal old-age pension age. This is because the cost of disability pension for any employee who is close to pensionable age is generally relatively small.

| Contribution category | Mean risk ratio of two years | Coefficient |

|---|---|---|

| 11 | Over 5 | 5.5 |

| 10 | 4.00–4.99 | 4.00–4.99 |

| 9 | 3.00–3.99 | 3.00–3.99 |

| 8 | 2.50–2.99 | 2.50–2.99 |

| 7 | 2.00–2.49 | 2.00–2.49 |

| 6 | 1.50–1.99 | 1.50–1.99 |

| 5 | 1.20–1.49 | 1.20–1.49 |

| Base category 4 | 0.80–1.19 | 1 |

| 3 | 0.50–0.79 | 0.65 |

| 2 | 0.20–0.49 | 0.35 |

| 1 | Under 0.2 | 0.1 |

Expense loading discount

From the start of 2023, the expense loading component of TyEL insurance contributions will be linked to the specific pension provider in question. The expense loading component is intended to cover the business expenses of the pension insurance company. Making the expense loading component company-specific will bring transparency to TyEL insurance contributions.

The expense loading fee will be determined on the basis of the individual customer company’s payroll and is added to the TyEL basic contribution rate. The larger the company’s payroll, the smaller the fee. If a company belongs to a group that is insured by Veritas, the fee will be determined on the basis of the payroll for the entire group.

The expense loading fee is set to correspond as closely as possible to Veritas’ estimated business expenses. The fee is smaller than the earlier general fee. Veritas’ expense loading fee is collected as part of the pension contributions paid from salaries. The expense loading discount is taken into account automatically in contributions and will be shown in the invoice as a smaller overall payment percentage.

Premium loss discount

The TyEL insurance contribution includes a premium loss component used to cover credit losses caused by unpaid insurance contributions to the pension provider. A premium loss discount is applied to the contributions of large employers.