The contribution category model for large employers underwent a reform at the beginning of 2024. The purpose of the reform is to promote the employment of those over the age of 55 or those with a partial work ability. The reform also aims to encourage employers to help maintain the work ability of their employees and to support coping at work.

The changes will be reflected in employers’ pension insurance contributions in future years.

What will change?

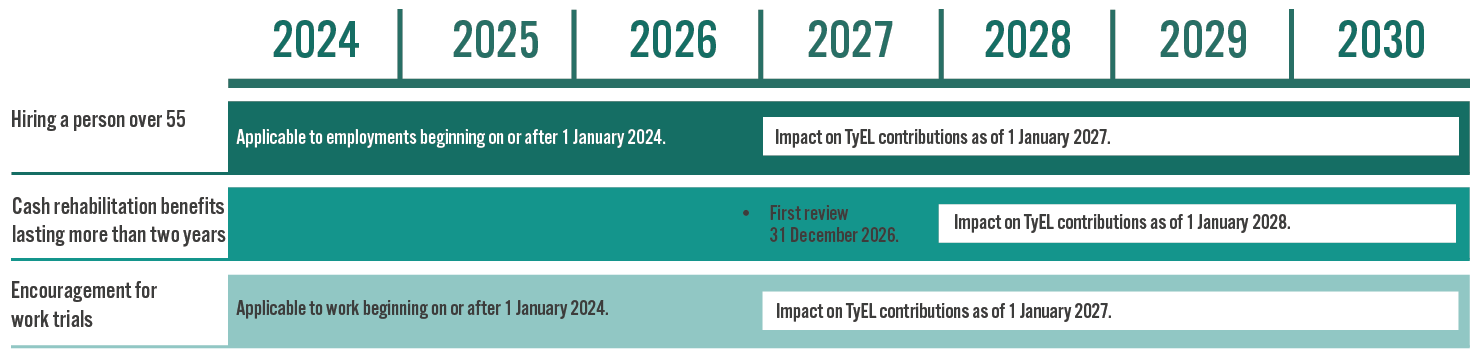

Hiring a person over 55

The disability of a person who was hired as a new employee over the age of 55 will not have an impact on the contribution category. The change applies to employment relationships that begin on or after 1 January 2024. Any change in the contribution category will be realised, at the earliest, in 2027.

Please note: An employee is not considered a new employee if they have worked for the same group of companies during the three previous years. The employer should ensure that the information concerning new employees can be found in the company’s HR system. If an employee develops an inability to work, the employer must remember to notify the pension provider of this as soon as possible. The notification must be made no later than by 15 November of the year following the year in which the employee retired on disability pension in order to avoid the impact of the contribution category.

Cash rehabilitation benefits that have continued for longer than two years affect the contribution category

An employee’s cash rehabilitation benefit will affect the employer’s contribution category if it has continued for longer than two years and no active rehabilitation measures are underway at the end of the two year period.

The change seeks to encourage employers to invest in rehabilitative measures at as early a stage as possible.

The cash rehabilitation benefits will be taken into consideration in the risk ratio for the first time in 2026, and they can impact the contribution category in 2028 at the earliest. If a person is granted disability pension until further notice after a cash rehabilitation benefit that affects the contribution category, the disability pension will no longer affect the contribution category.

Disability in employment relationships that began as vocational rehabilitation

If the employee’s employment relationship started with a work trial or apprenticeship training as part of vocational rehabilitation, the possible disability will not affect the employer’s contribution category. The protection period is valid for five years and is applicable to employment relationships starting on 1 January 2024 or later.

Cash rehabilitation benefits will be taken into account, for the first time, in the risk ratio of 2026. The risk ratio will, thus, impact the employer’s contribution category in 2028 at the earliest.

If an employee develops an inability to work, the employer must remember to notify the pension provider of this as soon as possible. It is the employer’s obligation to report that the employee’s employment relationship started with a work trial or apprenticeship training as part of vocational rehabilitation a maximum of five years prior to the pension contingency. The notification must be made no later than by 15 November of the year following the year in which the employee retired on disability pension in order to avoid the impact of the contribution category.

There will be no impact on the contribution category if the pension event was more than five years earlier

Disability pensions or cash rehabilitation benefits will not impact the company’s contribution category if the pension event was more than five years earlier. These pension events will not, as of 2026, be taken into consideration in the risk ratio that affects the employer’s contribution category. The 2026 risk ratio will affect the contribution category for 2028 and 2029.

The liability rate will decrease gradually

The employer’s liability rate for disability pensions will decrease gradually from the current level to 60 percent by 2028. This reduction applies to all employers. If an employer’s liability rate in 2024 was, for example, 10 per cent, it will be 6 per cent in 2028.

The maximum liability rate will be reduced by 10 percentage units per year over the years 2025–2028.

Employers’ disability pension contribution will change as a result of the reduced liability rate. The disability contribution of companies with higher contribution categories (5–11) will decrease. The disability contribution of companies with lower contribution categories (1–3) will increase as the reducing impact of the contribution category is decreased. The contribution for those with contribution category 4 will not be affected.

In order to ensure that the impact of the change will not radically and rapidly change contribution amounts, the reduction of the liability rate will be implemented in stages over a four-year period.

The impact of short employment relationships on the contribution category will be reduced

There will be no impact on an employer’s contribution category, even if an employee develops an inability to work, if less than EUR 10,000 was paid for the employment relationship in the two years preceding the contingency year marking the onset of the employee’s disability (at the 2022 level). The change concerns pension contingencies occurring on or after 1 January 2024.