The central labour market organizations reached a consensus on the pension reform just over a week ago. The government approved the proposal and considered that it meets the set goals for the reform. However, public discussion has raised concerns that the younger generation will bear the risks of the reform. Is this the case?

This time, the pension reform particularly affects the investment of pension funds. With the reform, pension insurance companies can increase the share of equity investments in their portfolios by about 10 percentage points. Currently, the equity weights of pension companies are on average slightly over 50 percent of the investment portfolio. Internationally, a 60 percent equity weight is not at all unusual.

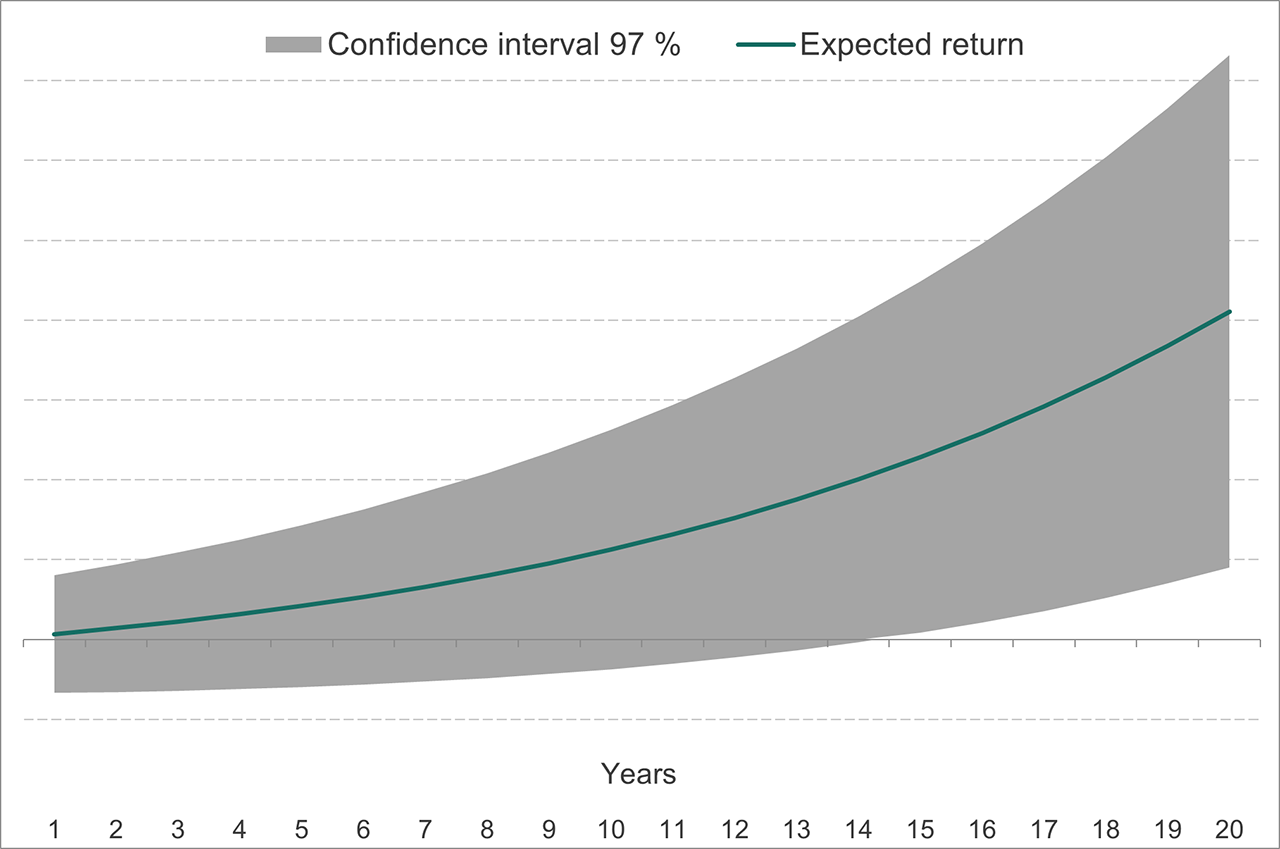

What happens to returns?

How does increasing the equity weight affect the overall return on pension funds? In the long term, the primary way to increase return expectations is to increase equity risk. This suits pension insurance companies, whose investment horizon spans decades. Higher equity risk thus means higher return potential in the long term. As a result of the changes, the return expectation for pension insurance companies would increase by about 0.3 percentage points from the current level.

However, investing is not that straightforward. Increasing the equity weight also means greater return variability, i.e., uncertainty about returns in the shorter term. In good times, returns are better than currently, and in bad times, they are worse.

Illustration of the impact of increasing equity weight on returns

Therefore, a higher equity weight requires better capacity to bear risk from the investor. Ensuring the pension system’s risk-bearing capacity in challenging market conditions is also essential in pursuing higher returns.

Risk-bearing capacity enables long-term investment activities

The pension system’s risk-bearing capacity is strengthened in the reform by lowering the solvency limit from the current 97 percent to 95 percent. This change means that the system better tolerates the fluctuations in returns caused by a higher equity weight. The goal of the change is to mitigate procyclicality, so pension companies do not have to sell their investments in market fluctuations.

The change in the solvency limit also improves pension investors’ risk-bearing capacity for other asset classes, and it allows for diversification in the investment portfolio. Increasing the equity weight means that the weight of other asset classes in the investment portfolio decreases. Various bond investments, alternative investments, and real estate still offer opportunities to diversify the investment portfolio’s risk.

This brings us to the third important change, namely leveraging real estate investments. It is typical for institutional investors to use leverage in real estate investing. Leverage means that real estate investments are financed with borrowed capital, such as loans from banks, in addition to equity. Previously, pension companies were allowed to use leverage only in real estate fund investments and to a limited extent in rental housing investments. The reform extends the use of leverage to all real estate investments. This change frees up capital for other investments.

Future prospects

The investment reform benefits younger generations because it increases the likelihood that pension contributions will not need to be raised in the future despite of the declining birth rates.

The pension reform also strengthens the funding of old-age pensions that works towards same goal: to increase pension funds and reduce the need for future pension contribution increases.

A higher return expectation investment strategy requires long-term commitment. It is essential to adhere to the chosen strategy despite unfavourable market conditions. Future generations will benefit from the increased likelihood of higher investment returns.

Also read:

What does the pension reform mean for Veritas customers? (29 January 2025)